The Health Insurance Marketplace (a.k.a. Health Insurance Exchange) will be open for enrollment beginning October 1, 2013, and people in the United States will be able to access the Health Insurance Marketplace beginning January 1, 2014. Currently, preparations are underway for the establishment of the Marketplace. In fact, FY2013 spending on the creation of the Marketplace could reach $1.5 billion this year. Despite this, funding challenges await full implementation of the health care marketplaces. (1-3)

A Few Facts – Health Insurance Exchange Future Individual Member Demographics: (4-7)

- Median age of 33

- Median income at 238% of the federal poverty limit

- 76% No college degree

- 56% Employed full-time

- 62% Unmarried

- 19% Do not speak English as a first language

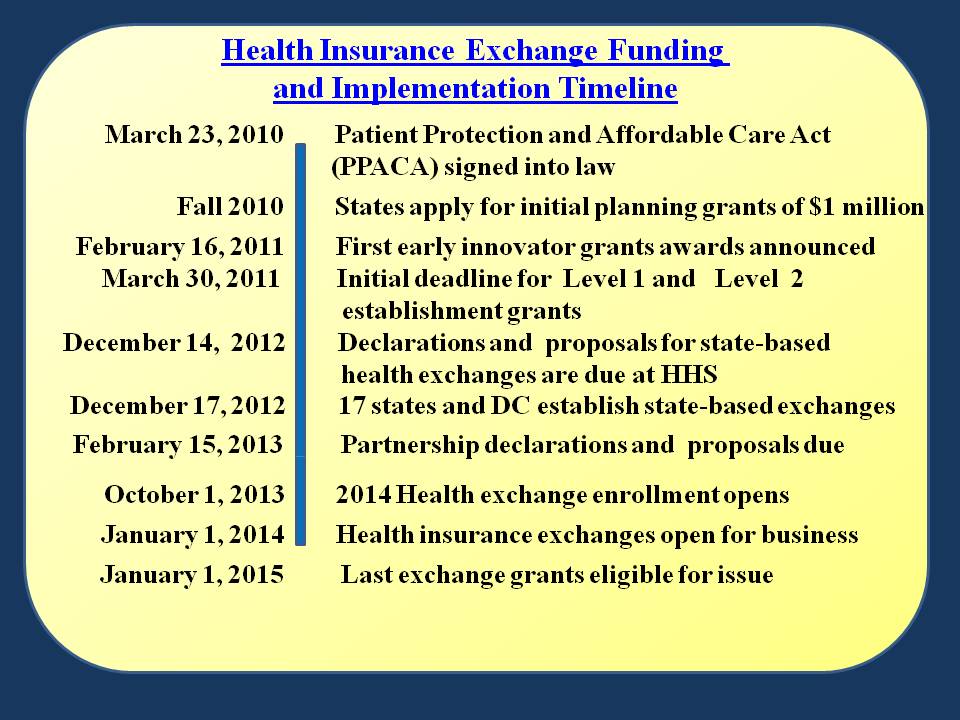

Where Are We Now, and How Did We Get Here?

Chart Source: Created using data from the Congressional Research Service and the Center on Budget and Policy Priorities (8, 9)

The Basics: What are the Health Insurance Marketplace Options?

There are three different options for health care exchanges: 1) federally-run, 2) federal-state partnerships, or 3) state-based. Twenty-seven states will operate federally run exchanges, having opted to participate by default due to their decision not to participate in state-based exchanges. Seventeen states and the District of Columbia will operate state-based marketplaces. The remaining seven states will run partnership exchanges. (8, 9)

A web interactive feature created by the Kaiser Family Foundation, “State Decisions For Creating Health Insurance Exchanges, as of May 28, 2013,” provides updated information regarding states’ election of one of the three health care exchange options listed above. (10)

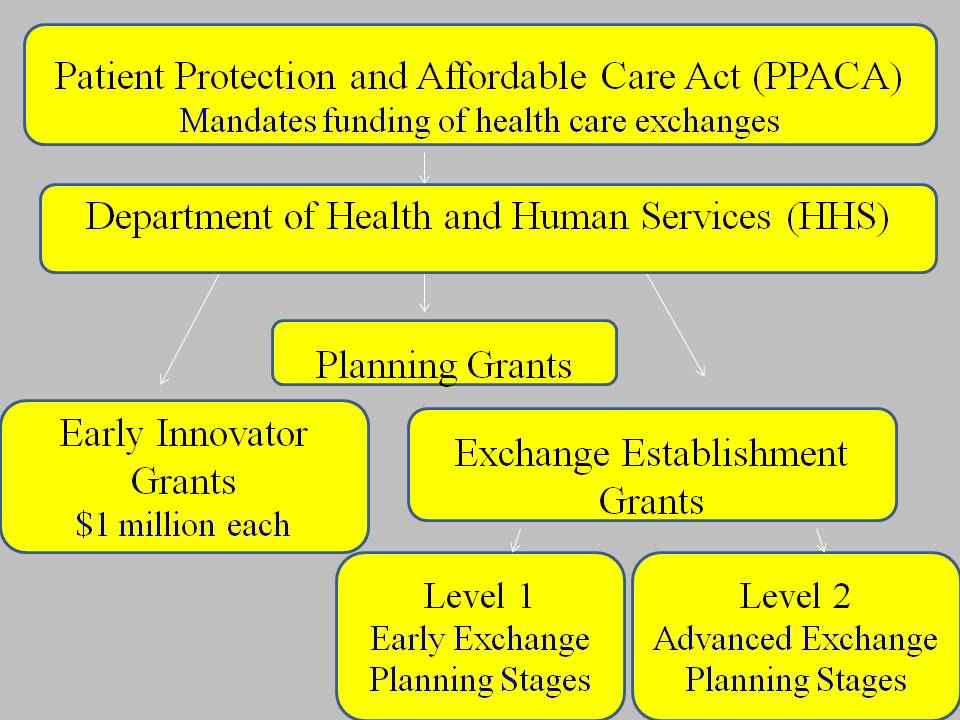

Federal Grant Funding for the Exchanges

As mandated by the Patient Protection and Affordable Care Act (PPACA), the Department of Health and Human Services (HHS) facilitates federal funding of health insurance exchanges. Three types of grants provide assistance to states in this capacity: planning grants, exchange establishment grants, and early innovator grants.

Chart Source: Created using data from the Congressional Research Service (8)

Forty-nine states, the District of Columbia, and several territories pursued planning grants of $1 million each to get their health insurance exchange ideas off the ground. Exchange establishment grants are of two types: Level 1 and Level 2. Level 1 grants offer assistance to states in the early stages of planning for the establishment of health marketplace exchanges. States can then apply for Level 2 funding after meeting certain eligibility criteria. Level 2 grants offer assistance to states in the more advanced stages of health exchange planning. according to a recent Congressional Research Service Report, “Status of Federal Funding and Implementation of Health Insurance Exchanges,” as of April 8, 2013, $3.6 billion in marketplace establishment grant funding had been awarded to 35 states and the District of Columbia. One third of the states receiving funding obtained both level 1 and level 2 funding. Information technology (IT) support is needed to ensure that the health exchanges are running smoothly. Early innovator grants serve to help supply this support. So far, seven of these types of grants have been awarded to individual states. (8)

Health Insurance Marketplace Funding and the President’s 2014 Budget

Again, funding of the preparation phase for the Health Insurance Marketplace is inadequate. The President’s 2014 Budget requests an additional $1.5 billion to finance federally-run and federal partnership health insurance marketplaces in 2014. A request for $2 billion is included for the support of state grants. The projected total amount of spending on both federal and state-run health insurance marketplaces is $4 billion. (3) A recent article claims that Secretary of Health and Human Services Kathleen Sebelius has requested funding from private entities to supplement government funds during the establishment and enrollment phase of the health care marketplaces. (11) Will this halt the effort? Not likely. It will just make implementation a bit more challenging than anticipated.

References

1. “What’s Changing and When: Open Enrollment in the Health Insurance Marketplace Begins” http://www.healthcare.gov/law/timeline/. Department of Health and Human Services. Retrieved June 2, 2013.

2. “Establishing the Health Insurance Marketplace” http://www.healthcare.gov/law/timeline/. Department of Health and Human Services. Retrieved June 2, 2013.

3. Carey, Mary Agnes. “HHS Seeking $1.5B In Funding To Run Federal Health Insurance Exchanges.” Kaiser Family Foundation Website. April 11, 2013. http://www.kaiserhealthnews.org/stories/2013/april/10/obama-budget-insurance-exchanges.aspx. Retrieved June 2, 2013.

4. PwC HRI Analysis for Year 2021

5. Current Population Survey

6. Medical Expenditure Panel Survey

7. Congressional Budget Office (CBO)

8. Mach, Annie L; Engler, Alex C; Redhead, C. Stephen. “Status of Federal Funding for State Implementation of Health Insurance Exchanges.” Congressional Research Service. May 8, 2013.

9. “Status of State Health Insurance Exchange Implementation.” Center on Budget and Policy Priorities. March 29, 2013.

10. “State Decisions For Creating Health Insurance Exchanges, as of May 28, 2013.” Kaiser Family Foundation. Website. http://kff.org/health-reform/state-indicator/health-insurance-exchanges/. 2013. Retrieved June 3, 2013.

11. Kliff, Sarah. ” Budget request denied, Sebelius turns to health executives to finance Obamacare.” The Washington Post. May 10, 2013. http://www.washingtonpost.com/blogs/wonkblog/wp/2013/05/10/budget-request-denied-sebelius-turns-to-health-executives-to-finance-obamacare/. Retrieved June 3, 2013.

5 Comments